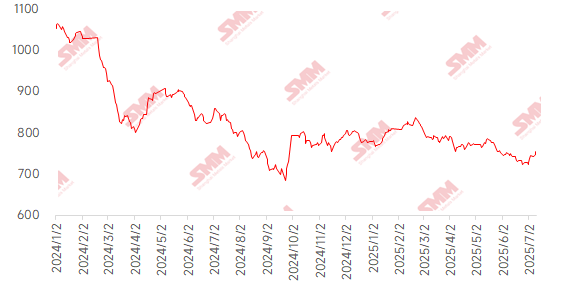

This week, imported iron ore prices showed a strong upward trend, with the price center significantly rising. At the beginning of the week, market sentiment weakened due to tariff policy expectations, and the futures market faced pressure with a slight drop. However, as the tariff implementation was postponed, market sentiment gradually recovered. From a supply and demand perspective, supply side, affected by the end of quarter-end push for targets and maintenance at some mines, global iron ore shipments dropped 12.27% WoW, showing a phased contraction. Demand side, although some steel mills arranged maintenance due to production restrictions, pig iron production at blast furnaces saw limited declines under the support of good profitability at steel mills, maintaining overall demand resilience. Notably, total inventory of the five major steel products this week showed an unseasonal buildup, disproving the earlier market concerns about negative feedback logic and further strengthening bullish expectations, driving a significant rally in iron ore futures prices. For port spot prices, the weekly average price of PB fines at Shandong ports rose 15-20 yuan/mt WoW.

Chart: SMM 62% Imported Ore MMi Index

Data source: SMM

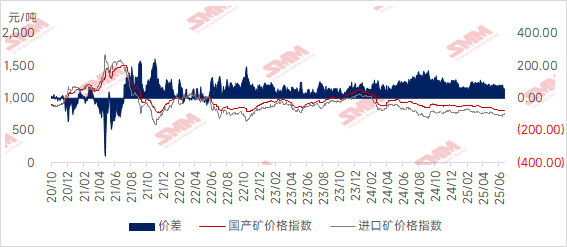

This week, domestic ore prices showed mixed performance. Domestic iron ore concentrates prices are expected to have some upward potential next week. In Tangshan, Qian'an, and Qianxi in Hebei, prices rose 5-10 yuan, while in west Liaoning, Chaoyang, Beipiao, and Jianping, prices increased 5-10 yuan/mt. East China also saw price increases of 5-10 yuan.

The domestic ore market in Tangshan, Hebei, remained stable overall. Currently, the ex-factory price of Fe66% iron ore concentrates on a dry basis including tax is 870-880 yuan/mt. Most traders considered steel mill order demand, with limited confidence in price increases. Buyers maintained a cautious approach in inquiries, unwilling to purchase above psychological expectations. Steel mills continued to purchase as needed, with a strong desire to drive down prices.

The domestic ore market in west Liaoning showed strong wait-and-see sentiment, with low operating rates at mines and beneficiation plants. In-production mines and plants had low willingness to sell at low prices, maintaining firm offers. The ex-factory price of Fe66% iron ore concentrates on a wet basis excluding tax was 670-680 yuan/mt. Traders and steel mills showed strong wait-and-see sentiment, with some steel mills expressing bearish views on the market outlook and a strong desire to drive down prices. Purchases were mainly as needed, with overall market transactions relatively sluggish.

In east China, mines and beneficiation plants mostly maintained normal production, selling as they produced, with inventory pressure significantly reduced. However, some mines and plants underwent routine maintenance this week, leading to a slight decline in local iron ore concentrates production.

Chart: Price Spread Between Domestic and Imported Ore

Data source: SMM

Next week's outlook:

For imported ore, the iron ore market is expected to show a sideways movement. Supply side, as seasonal maintenance at overseas mines ends, shipments are expected to rebound slightly with limited growth, and port inventories may fluctuate rangebound. Demand side, SMM data indicates that the impact of blast furnace maintenance is limited. Steel mill profits are moderate enough to support production enthusiasm, and pig iron production is expected to increase slightly, with the resilience of iron ore demand remaining. From a macro perspective, as the July Political Bureau meeting approaches, market expectations for "anti-cut-throat competition" policies and increased infrastructure investment have heated up, potentially boosting overall sentiment in the ferrous metals series. However, after the rapid rise in ore prices this week, market fear of high prices has emerged, with some long positions choosing to take profits, increasing the risk of short-term technical corrections.

Domestic ore perspective: Overall, the current domestic iron ore concentrates market is relatively quieter compared to the imported ore market, with steel mills generally having a strong desire to bargain down prices. However, this week, imported ore prices have risen significantly, improving the cost-effectiveness of domestic ore. Coupled with the fact that pig iron production from blast furnaces at steel mills remains at a relatively high level, providing some support for the demand for iron ore concentrates, and the recent strong trend in the iron ore futures market, it is expected that domestic iron ore concentrates prices may have some upside potential in the short term.

》Click to view the SMM Metal Industry Chain Database

![[SMM Hot-Rolled Coil Daily Trading] Spot Cargo Trading Volume Changed Narrowly](https://imgqn.smm.cn/usercenter/JAnHq20251217171716.jpg)